- Mar 28

Most of Your Close Isn't Waste. It's Worse: It's Misclassified.

- Arnaud Lemaire

- Accounting & Auditing

- 0 comments

If you've done any process improvement work on your month-end close, someone has probably asked you to classify tasks as "value-add" or "waste." Two buckets. Simple. That framework breaks in finance within five minutes. This article explains why, and what to use instead.

In the previous article, we mapped 127 close tasks across seven phases using SIPOC and found that 38.6% of total hours were value-add. Some people were surprised it was that low. Others said theirs would be worse. But the stat alone doesn't help you. Knowing that 61.4% of your close hours aren't value-add is a diagnosis, not a treatment. The real question is: what do you do with the other 61.4%?

Why two buckets don't work

In manufacturing, the binary split works because the test is physical. Does this operation change the shape, form, or function of the product? Yes: value-add. No: waste.

Try that on a month-end close. Your SOX bank reconciliation doesn't change a balance. It confirms what's already in the GL matches the bank. By the strict Lean definition, that's non-value-add. So is your control testing. So is your audit trail documentation.

Now go tell your controller you've classified the SOX reconciliation as waste.

You won't. Nobody does. So teams doing process improvement protect everything that feels important. Compliance work gets lumped in with value-add. The "waste" bucket ends up holding only the obvious stuff: duplicate entries, reports nobody reads, manual steps that should have been automated years ago.

The 40-50% of hours sitting in compliance and controls? Untouched. The framework gave people nowhere honest to put them.

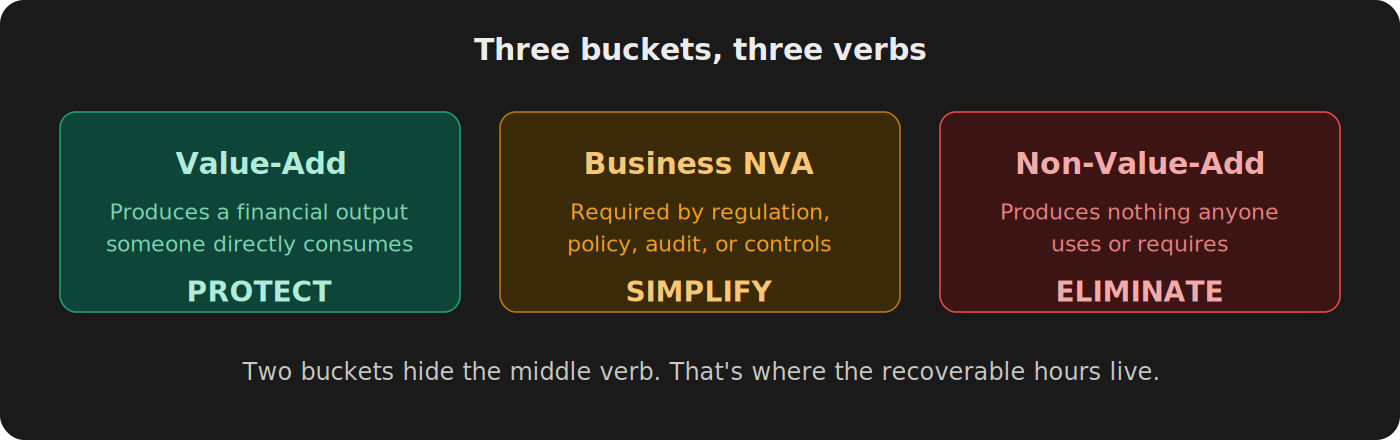

Three buckets, three verbs

The fix is a third category. In Lean Six Sigma, it's called Business Non-Value-Add (BNVA).

Value-Add (VA): The task produces a financial output that a reviewer, decision-maker, or regulator directly consumes. The revenue accrual in the P&L. The trial balance the controller reviews. Protect it.

Business Non-Value-Add (BNVA): Required by regulation, policy, audit, or internal controls, but doesn't directly produce a financial output someone reads. Your SOX reconciliation. Your control sign-offs. Your approval routing. You're keeping it. But spend the minimum time necessary. Simplify it.

Non-Value-Add (NVA): Produces nothing anyone uses. No reviewer reads it, no regulator requires it, no decision depends on it. Eliminate it.

Protect, simplify, eliminate. When you force everything into two buckets, the middle verb disappears. And that's where most of the recoverable hours live.

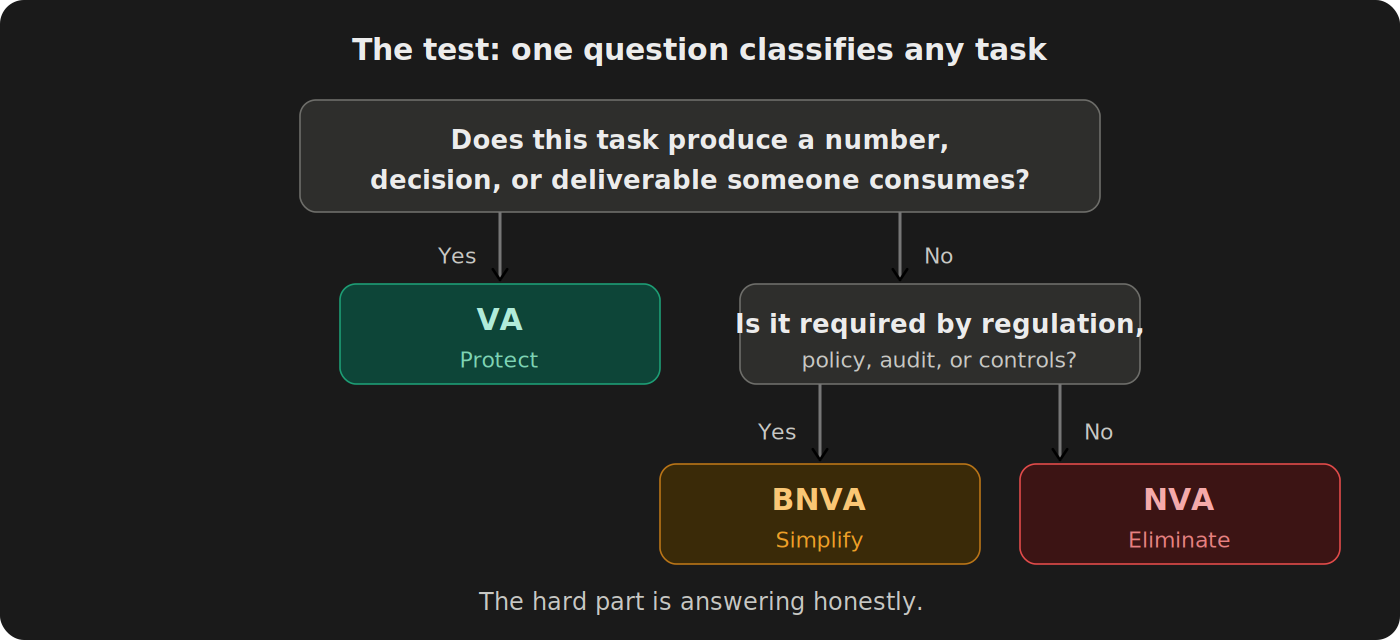

The test, applied to three real tasks

One question classifies any close task:

Does this task produce a number, a decision, or a deliverable that a reviewer or regulator directly consumes?

Yes: VA. Required but no: BNVA. Neither: NVA.

Simple enough. The hard part is answering honestly. Here are three tasks from a manufacturing close where teams argue.

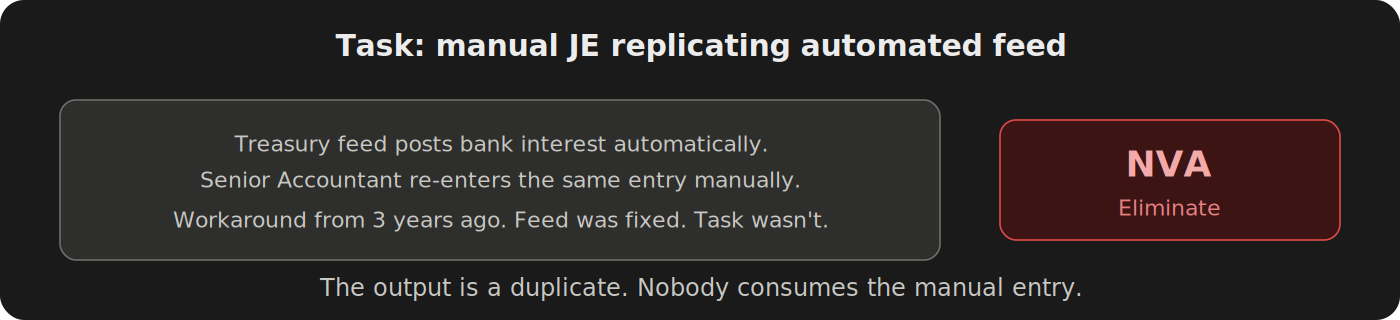

Task 1: Manual journal entry replicating an automated feed

Every month, the Senior Accountant downloads the bank interest calculation from Treasury's system and re-enters it as a manual journal entry in the GL. The ERP already has an automated feed from the Treasury module that posts the same entry. The manual one exists because three years ago the feed was broken for two months, someone built a workaround, the feed got fixed, and nobody turned off the workaround.

NVA. The output is a duplicate. Nobody consumes the manual entry. Eliminate it.

This one's easy. The next two aren't.

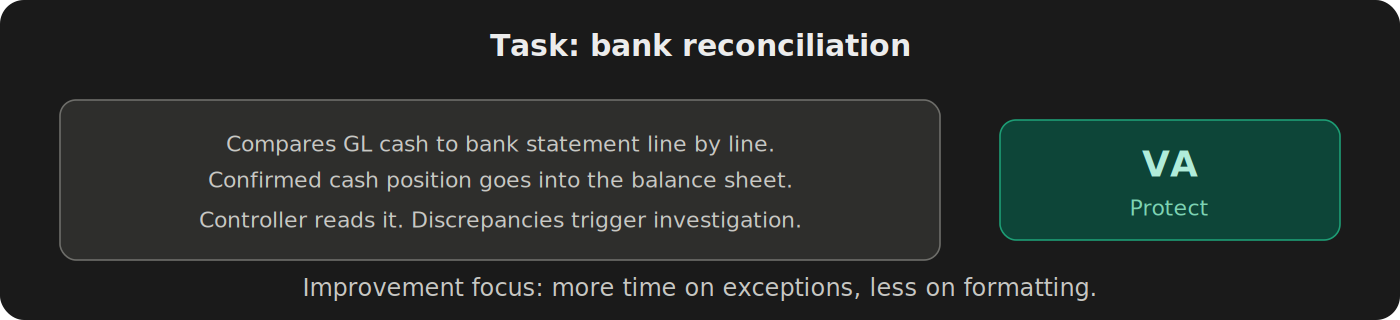

Task 2: Bank reconciliation

The reconciliation compares the GL cash balance to the bank statement, line by line. It identifies timing differences, uncleared items, and discrepancies.

First instinct for a lot of people: BNVA, because it's a control. But ask the test question. Does it produce a number someone directly consumes? Yes. The confirmed cash position goes into the balance sheet. The controller reads it. If there's a discrepancy over threshold, it triggers an investigation and potentially an adjustment.

VA. The improvement effort here isn't about cutting time. It's about making sure the hours go to investigating exceptions rather than formatting the output into a template nobody asked for.

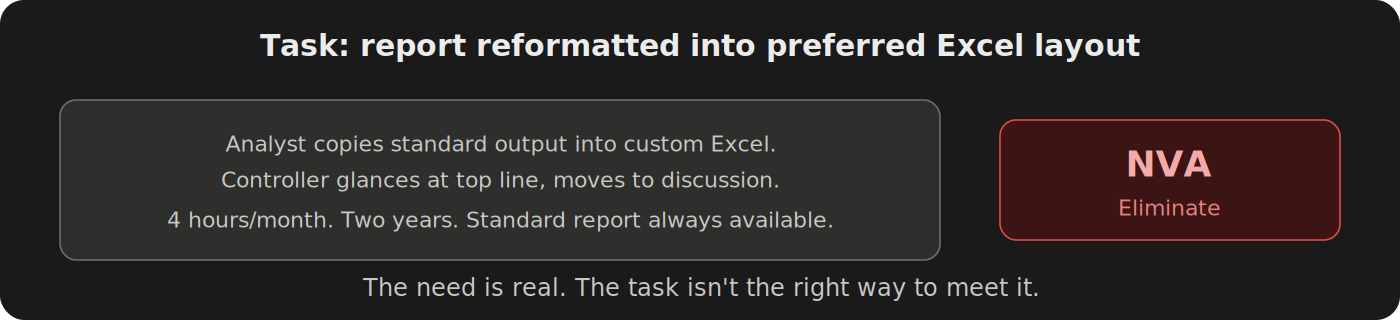

Task 3: Monthly management report reformatted into the controller's preferred Excel layout

Every month, the financial analyst takes the standard output from the reporting tool, copies it into Excel with custom headers, color-coded rows, and a specific sort order the controller prefers. The controller opens it at the start of the review meeting, glances at the top line, and moves to the discussion.

This one feels like BNVA. The controller expects it. It's part of the rhythm.

Apply the test. Does the reformatted report produce a number that doesn't already exist? No. Does a regulator require this format? No. Does the controller make a decision from this layout that they couldn't make from the standard output? If you ask honestly: no.

NVA. The original report exists. The reformatting adds presentation, not information. Eliminate the step. If the controller needs a specific view, that's a reporting tool configuration, not a recurring manual task.

I used this exact example in a classification workshop once. The analyst pushed back immediately: "But he's asked for it every month for two years." Right. And in those two years, the standard report was always available. What the controller wanted was a familiar format. What the analyst gave him was four hours a month of habit maintenance dressed up as a deliverable.

The three-way split gave us the language to have that conversation without telling the analyst their work was useless. BNVA would have meant: we keep it but simplify it. NVA means: the underlying need is real (the controller wants a clear view), but this specific task isn't the right way to meet it.

That's the difference the third bucket makes. It forces a better conversation.

What your team will say (and what's actually going on)

If you run this exercise with your team, the resistance is predictable. Not because people are lazy or defensive, but because the classification asks them to do something uncomfortable: question work they've been doing on autopilot.

"Everything I do is required." I heard this from a plant controller who had 14 reconciliation tasks on her close checklist. We went through them one by one. Three had regulatory backing she could cite. Four were in the company's internal controls matrix. The other seven? "Well, my predecessor set them up." We traced two of those back to a one-time audit finding from 2019 that had been remediated. The recons kept running because nobody told them to stop. Seven tasks, required by nobody. That's not unusual. That's average.

"My manager expects this output." This one showed up at a group controlling site where the team produced a 40-page variance commentary deck every month. I asked who read past page 8. Silence. Then the team lead said: "The CFO reads the first three pages. The rest is for completeness." Completeness for whom? If 32 pages go unread every month and nobody notices, the expectation is an assumption, not a requirement.

"If I classify my tasks as NVA, I'm arguing myself out of a job." A cost accountant said this to me during a workshop at a chemicals plant. Fair concern. But we were looking at his task list and half of it was manual data pulling from SAP that a scheduled report could have replaced. When we eliminated those tasks, he didn't lose his job. He started doing variance analysis on raw material yields, something his manager had wanted for a year but nobody had the bandwidth. The NVA work was blocking the VA work. That's almost always the case.

"Our auditors need this." Sometimes true. Often an interpretation that grew over time. At one site, the team maintained a manual log of every intercompany transaction as a separate Excel file alongside the ERP data. When I asked why, the answer was "audit." When we asked the auditor, they said they pull the data from SAP directly. The log had been unnecessary for at least two years. Nobody had checked.

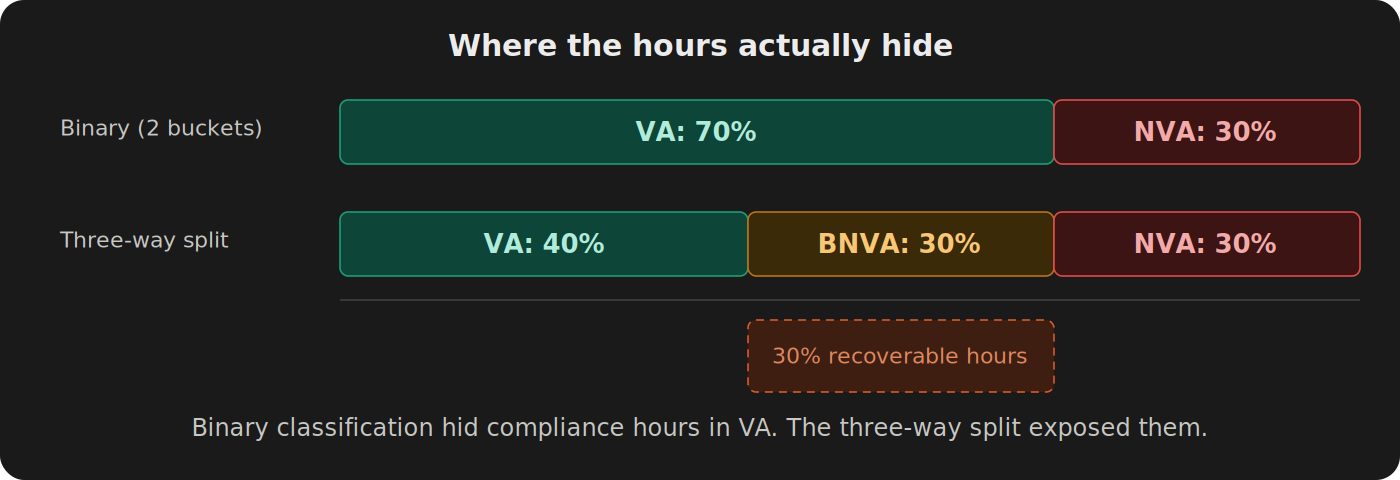

Where the hours actually hide

When you give teams only two categories, nobody classifies their own tasks as waste. The result is a classification that looks complete but changes nothing.

In one manufacturing close I ran, the team finished a classification exercise with a 70% VA ratio. When I sat with them and walked through the BNVA test on each task individually, the real number was closer to 40%. The gap: 30% of their close hours sitting in compliance and control tasks that were required but could be done in half the time. Binary classification had no place for them, so they defaulted to VA. The improvement effort never touched them.

This isn't surprising when you consider that only 30% of finance teams even have a documented close checklist. If 70% of organizations are running the close from memory, the idea that they've done a proper value classification is unrealistic.

BNVA gives people permission to say: "This is required. It doesn't produce a financial output. We're keeping it, but we're going to spend less time on it." That permission is where the hours come back.

Your VA ratio becomes a metric you can track. 38% this month. 42% after you eliminate three NVA tasks and simplify two BNVA workflows. The difference in hours has a dollar figure. That dollar figure is your business case.

The sequencing matters too. Eliminate NVA first: cheapest, fastest, least resistance. Simplify BNVA second: moderate effort, visible time savings. Protect and improve VA last: highest effort, highest impact, requires the most skill. Early wins fund the harder changes. I've watched teams spend weeks optimizing the formatting of a report that three people receive and nobody reads. That's what happens when you skip the classification and jump straight to improvement.

Classification as an AI readiness map

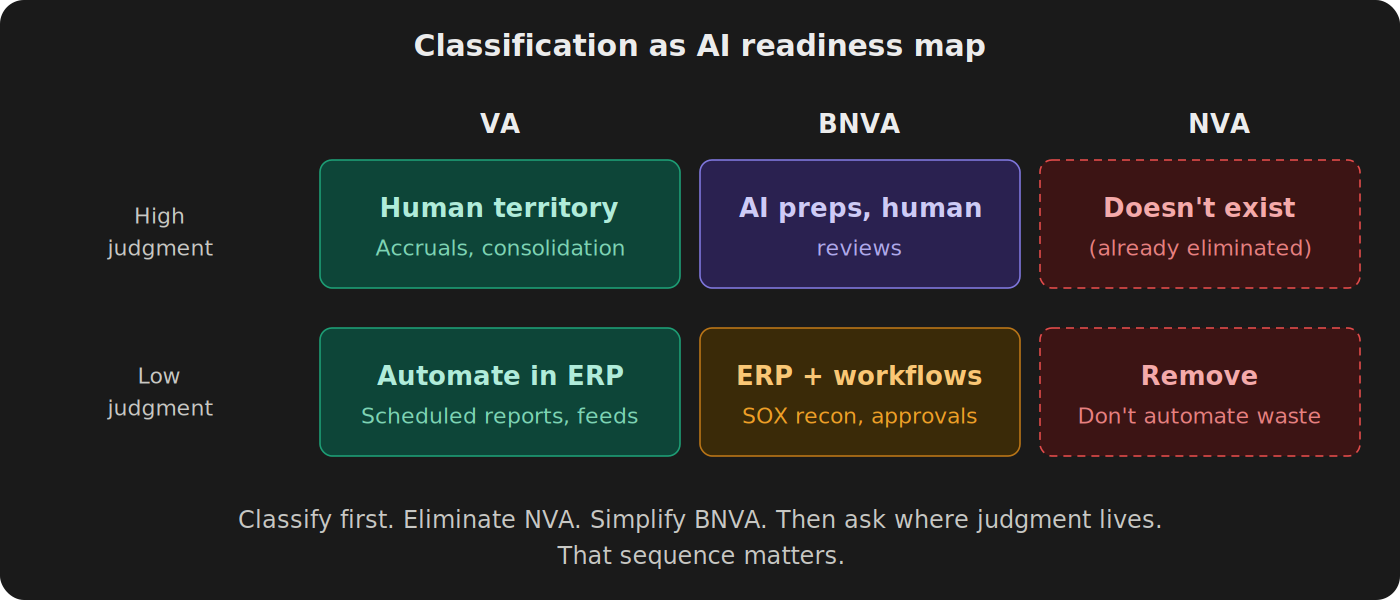

Once you've classified honestly, you've built something you probably didn't intend: a map of where human judgment actually matters.

VA tasks are where financial judgment lives. The accrual that requires an estimate. The consolidation adjustment where someone decides if the intercompany difference is timing or a real error. The quality of the person doing the work shows up directly in the output. High judgment. Human territory.

NVA tasks are elimination candidates. Period. You don't automate these with AI. You remove them. Automating a task that shouldn't exist is still waste. Just faster.

BNVA is where it gets interesting. Not all BNVA work carries the same judgment intensity. A SOX reconciliation has a defined procedure, a defined input, and a pass/fail output. An approval routing is a workflow. The person clicking "approve" isn't making a decision; they're confirming a condition was met. Low judgment. High repetition.

Compare that to reviewing a complex lease classification or validating the assumptions behind a provision estimate. Same bucket, completely different judgment intensity.

That distinction tells you where technology actually helps. Low-judgment BNVA doesn't need AI. It needs the ERP configuration and scheduled workflows that should have been set up properly years ago. High-judgment BNVA needs a person, but AI can prep the work: pull the data, flag outliers, draft the documentation. The person reviews instead of building from scratch.

If your organization is talking about AI in the close (and every organization is right now), start here. Classify first. Eliminate the NVA. Simplify the BNVA. Then ask where judgment lives. That sequence matters. Skip it and you'll spend six months building an AI workflow for a task that a scheduled ERP report could have replaced. Or for a task that shouldn't exist at all.

Try this before next close

Pick five recurring monthly tasks your team has been doing the same way for more than a year. For each one, answer the test question honestly. Write down VA, BNVA, or NVA.

If you find yourself arguing that something is VA because someone expects it rather than because it produces a financial output someone consumes, sit with that. That's the gap.

Five tasks won't change your close. But they'll change how you see the other 122.

What comes next

The SIPOC article mapped the close. This one classified it. Next question: once you know which tasks matter, how do you figure out which ones control your timeline? That's the critical path, and it's the next article in this series.

If you want to classify all 127 tasks across seven phases with auto-calculated ratios and a working tracker, that's Lesson 3 of the Month-End Close Optimization course on GoFast.Finance.

-> Month-End Close Optimization: 10 lessons, one working system

Frequently asked questions

What is the difference between BNVA and NVA? BNVA is required by a specific regulation, policy, or control you can name. NVA is required by habit. The test: if you stopped doing it tomorrow, would a regulator or auditor flag it within 12 months? If yes, BNVA. If nobody would notice, NVA.

Can a task change classification over time? Constantly. A report that was VA when a specific decision-maker consumed it becomes NVA the month they leave and nobody picks up the consumption. I've seen tasks drift from VA to NVA over two years without anyone noticing because the checklist kept running on autopilot. Review classifications at least once a year.

What's a realistic VA ratio for a month-end close? In the manufacturing closes I've mapped, honest VA ratios land between 35-45%. Teams that self-report with only two categories typically claim 65-75%. The gap is almost entirely compliance and control work that binary classification had nowhere to put. If your number is above 60%, you probably haven't introduced the third bucket yet.

Won't people resist classifying their own work as NVA? Every time. That's why the three-way split works better than the binary one. "Your task is waste" is a conversation nobody wants to have. "The need behind your task is real, but the task itself isn't the right solution" is a conversation people can have. The framework gives you language that's honest without being personal. The cost accountant who was afraid of losing his job ended up doing the work his manager actually wanted. The NVA tasks were in the way.

Sources

APQC General Accounting Open Standards Benchmarking Survey (2017) - 2,300 organizations surveyed. Median close cycle: 6.4 calendar days.

Ledge, "The State of Month-End Close in 2025" - 50% take 6+ business days to close. 94% still rely on Excel.

FloQast & University of Georgia, "Burnout in the Accounting Profession" (March 2022) - 81% say month-end close disrupts personal lives.

Eagle Rock CFO, "Month-End Close Benchmarks 2026" - Only 30% have a documented close checklist.

VA/BNVA/NVA classification - Standard Lean Six Sigma value classification methodology, documented across ASQ (American Society for Quality) references.

This article originally appeared in the Practical Lean Finance newsletter on LinkedIn.